Global Personal Loan Insights

This guide explores personal loans from banks in English-speaking countries. Analyzing offers from key lenders, such as rate structures, fees, and terms, will enhance your decision-making. The keyword 'PL 10762 2018' references standard protocols in financial transactions that can influence loan agreements.

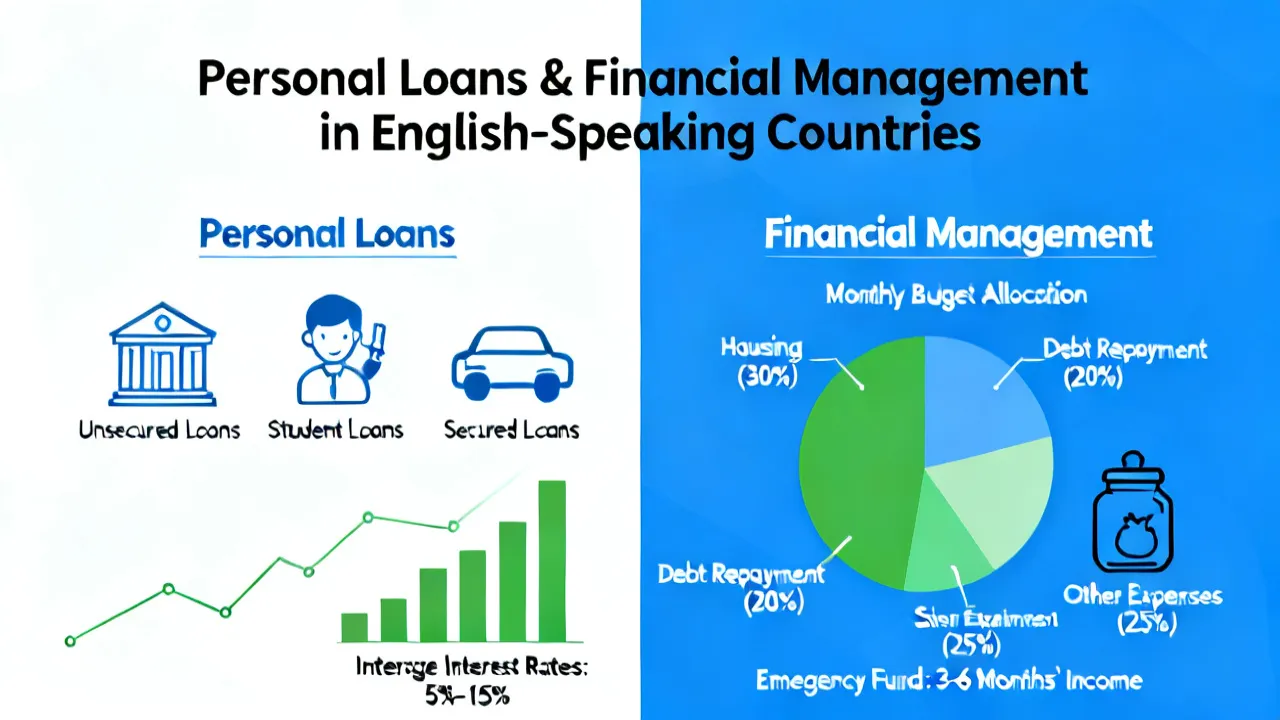

Understanding Personal Loans in English-Speaking Countries

Personal loans are crucial financial tools designed to cover expenses that range from consolidating debts to funding major purchases or untimely emergencies. These loans provide borrowers with the cash they require for various needs, which can include medical expenses, home renovations, travel, or education. The flexibility of personal loans makes them a popular choice among many consumers around the world. This article delves into personal loan offerings from several prominent banks in English-speaking countries, providing a detailed comparison to aid potential borrowers in their decision-making.

A Detailed Look at PL 10762 2018

'PL 10762 2018' serves as a standard or guideline involved in the financial regulatory framework that can influence how loan agreements are structured and managed. Understanding such standards is essential as they ensure that the terms and conditions in loan agreements meet consistency and fairness across the board. This legislation plays a crucial role in protecting consumers, ensuring they are informed about their rights and obligations when entering into loan agreements and minimizing the risk of predatory lending practices. By adhering to these guidelines, lenders can maintain a level of trust and transparency with their customers.

Analyzing Key Loan Options

Loan options across different banks offer a spectrum of choices tailored to various financial situations. The diversity in offerings provides consumers the opportunity to select loans that not only fit their immediate needs but also ensure manageable repayment terms and interest rates. Here, we look at a few noteworthy examples of personal loans available across English-speaking countries:

| Bank & Country | Annual Interest Rate | Loan Amount | Additional Fees | Repayment Period | Repayment Example |

|---|---|---|---|---|---|

| Harmoney (Australia) | From 5.76% p.a. | AUD 2,000–70,000 | Establishment fee up to AUD 575; no early repayment fee | 3, 5, or 7 years | AUD 20,000 over 5 years at 5.76% is ~$382/month |

| TD Bank (Canada) | From 8.99% p.a. (variable) | CAD 5,000–50,000 | Variable application fee; no early repayment penalties | 1–5 years | CAD 10,000 at 7.99% over 4 years is ~$244/month |

| Wells Fargo (United States) | 7.49%–23.74% p.a. | USD 3,000–100,000 | No origination fee; late fee may apply | 12–84 months | USD 20,000 at 6.99% over 5 years is ~$396/month |

It is essential for borrowers to compare interest rates and fees associated with these loans, as they can significantly impact the total cost of borrowing. Depending on individual financial situations, the choice of lender may also be influenced by factors such as customer service, ease of application, and the reputation of the institution.

Steps to Apply for a Loan

The process to apply for a personal loan in these countries is generally straightforward but varies slightly based on local regulations and bank policies. Following a structured approach can help streamline the application process. Here are the key steps:

- Assess Financial Needs: Before approaching a bank, it is vital to determine the loan amount needed and the loan's purpose. Creating a detailed budget can help evaluate how much can be borrowed without straining personal finances.

- Research Lenders: Take time to compare the terms, interest rates, and fees from various banks. Many lenders provide online tools that make it easier to check and compare rates instantly.

- Pre-Qualification: Utilize online tools provided by banks to check eligibility without affecting your credit score. Pre-qualification offers a glimpse into potential loan terms based on the initial information provided.

- Gather Required Documentation: Prepare necessary documents that will verify identity, income, and creditworthiness. Typical requirements include identification documents, proof of employment, recent pay stubs, bank statements, and possibly tax returns.

- Submit Application: Personal loan applications can often be completed online, or you may opt to visit a branch. Ensure that all sections are filled accurately to avoid delays.

- Verification and Approval: After submission, the bank will conduct a review of the application and supporting documents, and the final decision will either approve or deny the loan request.

- Accept Loan Offer: On approval, review the loan agreement vigorously, paying attention to interest rates, repayment terms, and any additional fees before accepting the offer and proceeding with the loan disbursal.

It is crucial at this stage to ask questions if any part of the loan agreement is unclear. Understanding all terms and conditions before accepting a loan ensures that there are no surprises in the future.

FAQ Section

- What credit score is needed for a personal loan? Banks generally prefer a good-to-excellent credit score for unsecured loans, but specific requirements vary per institution. Most lenders typically look for a score of around 600 or higher, but the threshold can be different based on the lender's criteria and the loan type.

- Can loans be repaid early without penalty? Many banks, like SoFi and Harmoney, offer loans with no early repayment fees, boosting financial flexibility. Borrowers should check if their lender has any stipulations regarding early repayments, as some may impose penalties.

- What dictates the interest rate on a personal loan? Factors such as the applicant's credit score, loan amount, duration, and lender policies primarily influence interest rates. It is also essential to note that prevailing economic conditions and market interest rates can cause fluctuations in the rates offered.

- Are personal loans secured or unsecured? Most personal loans are unsecured, meaning they do not require collateral. However, secured personal loans may require an asset as collateral, typically offering lower interest rates due to reduced risk for the lender.

- How long does it take to receive funds after approval? The timeframe to receive funds can vary by lender but typically ranges from one day to a few weeks. Online lenders often provide quicker access to cash than traditional banks.

- Can I use a personal loan for any purpose? Generally, personal loans offer flexibility in usage. However, some lenders might impose restrictions, so it's best to check the terms regarding acceptable uses of the loan.

Disclaimer

1) The above information derives from various online sources, and all data is as of October 2023. 2) Specific loan requirements and repayment methods are subject to official bank policies and may change without prior notice. This website does not update real-time information.

Further Reading and References

- Harmoney Australia

- ANZ Bank

- TD Bank Canada

- RBC (Royal Bank of Canada)

- Lloyds Bank UK

- Santander UK

- Wells Fargo USA

- SoFi USA

The Importance of Credit Scores in Personal Loan Applications

One of the pivotal factors influencing the approval of personal loans is the borrower's credit score. Credit scoring is a numerical expression based on an analysis of the credit files of individuals, representing the creditworthiness of a person. Generally, the higher the score, the better the chances of obtaining a loan with favorable terms. Banks assess credit scores to evaluate the risk level associated with lending to a specific borrower, with scores generally classified in three tiers: poor, fair, and good to excellent. A strong credit history can significantly reduce interest rates and open up better borrowing options, while a low credit score may limit access.

Obtaining a free credit report prior to applying for a loan is an excellent first step for borrowers. This can help identify any inaccuracies that may be affecting the score and allow time for disputes to be resolved. Understanding your credit position enables you to make informed decisions about which loans to apply for and to negotiate terms more effectively.

The Impact of Loan Terms on Borrowers

Loan terms refer to the details of the loan agreement, including the length of time for repayment (known as the loan term), the interest rate, and any fees involved. Understanding these elements is vital for responsible borrowing. Loan terms determine monthly payment amounts and the total cost of the loan, and they can affect financial stability over the life of the loan.

Shorter loan terms typically result in higher monthly payments, but they reduce the cost of interest paid over the life of the loan. Conversely, longer loan terms induce smaller monthly payments but often lead to paying much more in interest over time. It is essential for borrowers to balance immediate cash flow needs with long-term financial health when choosing their loan terms.

Additionally, borrowers should be aware of any potential fees associated with their loan, including origination fees, pre-payment penalties, and processing fees. Understanding all potential costs empowers individuals to compare loan offerings accurately and make informed financial decisions.

Real-Life Scenarios: When to Take a Personal Loan

Personal loans can be beneficial in various financial scenarios, and understanding these situations can assist borrowers in making effective choices. Here are a few examples of when obtaining a personal loan might be a prudent decision:

- Debt Consolidation: If an individual is burdened with multiple high-interest debts, such as credit card debt, consolidating these into a single personal loan with a lower interest rate can simplify payments and potentially save money on interest.

- Medical Expenses: Unexpected medical emergencies can lead to significant financial strain. Personal loans can offer necessary support during these unforeseen circumstances by providing immediate cash flow to address medical bills.

- Home Improvements: Investing in home renovations can increase property value. A personal loan can fund necessary repairs or upgrades without draining savings or tapping into retirement funds.

- Major Life Events: Life-changing events such as weddings, graduations, or travel plans sometimes require additional funds. Personal loans can help finance these significant experiences, making them financially accessible.

- Education Expenses: Pursuing education or professional development can be costly, and personal loans can bridge the financial gaps associated with tuition, books, or living expenses.

In each scenario, evaluating the potential return on investment and the long-term impact of taking on debt is crucial. Borrowers should ask themselves if the benefits outweigh the costs associated with the loan.

Understanding the Fine Print: Loan Agreements and Documentation

Once a personal loan application is approved, the borrower receives a loan agreement that outlines the terms of the loan. It is critical to read this document thoroughly before signing. Key elements often found in loan agreements include:

- Loan Amount: The total amount being borrowed, which is crucial for assessing repayment capacity.

- Interest Rate: The cost of borrowing expressed as a percentage of the loan amount.

- Repayment Schedule: Information on how often payments are due and the duration of the loan.

- Fees: Details of any charges or fees that may apply, such as late payment penalties or origination fees.

- Prepayment Terms: Information on whether there are any penalties for repaying the loan early.

Borrowers should pay attention to these terms to avoid surprises later on. If any part of the agreement is unclear, it is advisable to consult with a financial advisor or speak directly with the lender to ensure all aspects of the loan are fully understood.

Exploring Alternatives to Personal Loans

While personal loans can serve as valuable financial instruments, they are not the only option available to borrowers. Various alternatives might be more suitable depending on individual financial circumstances and goals:

- Credit Cards: For smaller expenses, using a credit card can be an appropriate choice, allowing for flexible repayment. However, high-interest rates may become an issue if the balance remains unpaid for extended periods.

- Peer-to-Peer Lending: Platforms like Lending Club or Prosper connect borrowers with individual investors willing to fund loans. These platforms can sometimes offer more competitive rates.

- Home Equity Loans/Lines of Credit: Homeowners can leverage their assets to obtain loans against home equity. These options typically offer lower interest rates due to the secured nature of the loans, though they also carry risks.

- Payday Loans: It is essential to approach payday loans with caution. While they offer quick access to cash, they often come with exorbitant interest rates and fees, potentially leading to a cycle of debt.

Evaluating all options, including understanding the pros and cons, will help consumers choose the best financial products for their unique circumstances.

Final Considerations: Making an Informed Decision

In conclusion, obtaining a personal loan can be a straightforward process if approached with care and diligence. Knowledge of loan options, understanding the implications of borrowing, and careful analysis of one’s financial situation are all crucial components to successful loan management. Borrowers should spend time researching and comparing lenders, evaluating the impact of loans on their financial future, and reading the terms of agreements carefully.

By maintaining financial discipline and awareness of credit scores, individuals can responsibly utilize personal loans to enhance their lives, whether by consolidating debt, managing emergencies, or making significant investments in their futures. Personal loans can be a powerful financial tool when used wisely, providing the necessary resources to navigate life’s financial challenges and opportunities.

Further Reading and Resources

-

1

Explore the Tranquil Bliss of Idyllic Rural Retreats

-

2

Unlock the Full Potential of Your RAM 1500: Master the Art of Efficient Towing!

-

3

Leveraging High-Interest CDs for Optimized Investment Returns

-

4

How to Take Advantage of Debt Consolidation Loans: Key Strategies

-

5

Understanding Debt Consolidation Loans: Weighing Advantages and Disadvantages