Comprehensive Guide to Global Loan Options

This guide explores various loan services available in English and Japanese-speaking countries. The "56d Bet" primarily relates to betting or speculative investments requiring understanding and mitigation of risks. In financial terms, it translates to taking calculated risks, mirroring how selecting the right loan involves careful assessment of interest rates, repayment terms, and lender credibility.

Understanding the 56d Bet: A Financial Perspective

The term "56d Bet" is often linked with investment strategies involving calculated risks and predictions, similar to betting. In the financial world, particularly loans, it involves evaluating interest rates, repayment terms, and the stability of the lending institutions to make informed borrowing decisions. The concept can be expanded to illustrate how personal finance plays into our decision-making process, where we weigh benefits against potential pitfalls. Just as in betting, the objective is to maximize gains while minimizing losses, requiring a thorough understanding of all variables at play.

Global Loan Options for Savvy Borrowers

Loan services vary significantly across countries, influenced by economic policies, banking regulations, and consumer needs. In this guide, we'll explore loan offerings in English-speaking and Japanese-speaking regions, providing detailed comparisons and insights to empower potential borrowers with the knowledge to make strategic decisions. Such knowledge helps to create an informed borrower, capable of navigating complex financial markets and securing the best rates and terms available.

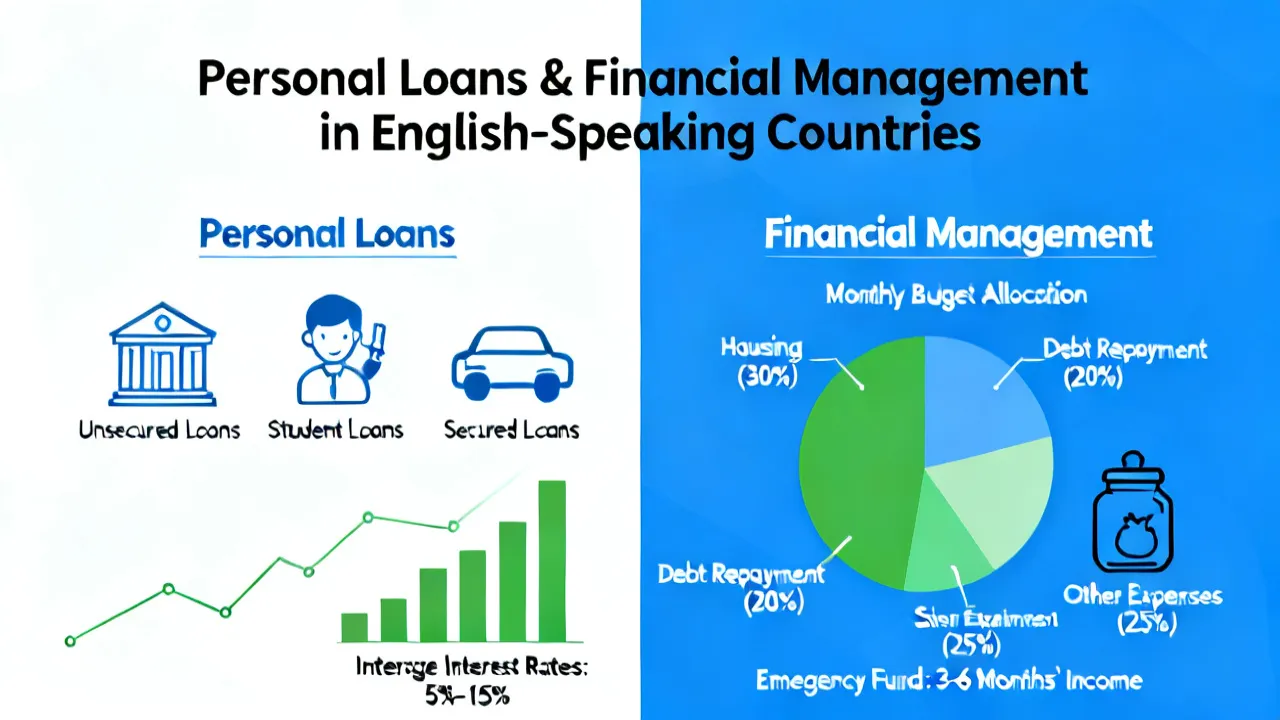

Loan Options in English-Speaking Countries

English-speaking countries, including Australia, Canada, the United Kingdom, and the United States, offer varied loan services tailored to different financial needs. For instance, some institutions provide unsecured loans, allowing individuals to borrow without collateral, whereas others offer secured options for larger sums. Understanding these options is paramount for borrowers aiming to leverage financial opportunities responsibly.

| Country | Institution | Details |

|---|---|---|

| Australia | Harmoney | Unsecured Loan: AUD 2,000–70,000, Interest Rate from 5.76% p.a. |

| Canada | TD Bank | Personal Loan: CAD 5,000–50,000, Variable rates starting at 8.99% p.a. |

| UK | Lloyds Bank | Fixed Personal Loan: £1,000–50,000, Interest Rate from 4.9% p.a. |

| USA | SoFi | Unsecured Loan: USD 5,000–100,000, Interest Rate 6.99%–21.99% p.a. |

source: [Harmoney](https://www.harmoney.com.au), [TD Bank](https://www.td.com/us/en/personal-banking), [Lloyds Bank](https://www.lloydsbank.com), [SoFi](https://www.sofi.com)

Understanding Loan Application Processes

Applying for Loans in English-Speaking Countries

The process of applying for a loan often involves evaluating one’s creditworthiness, understanding the loan terms, filling out application forms, and providing necessary documentation. Institutions may differ slightly in requirements, but the following steps are generally applicable:

- Step 1: Determine your loan amount and objective.

- Step 2: Research and compare lenders according to rates, terms, and customer reviews.

- Step 3: Prepare financial documents, such as proof of income, identification, and credit scores.

- Step 4: Submit an online or in-person application form; ensure to double-check all information for accuracy.

- Step 5: Await approval and carefully review the loan agreement before acceptance, ensuring you understand all terms, including hidden fees.

- Step 6: Post-acceptance; create a repayment plan considering your monthly budget.

Loan Offerings in Japanese-Speaking Regions

Japanese banks provide a range of loan services, typically requiring borrowers to demonstrate stable income and credit history. Interest rates can be competitive, with various options to suit personal and business needs. In Japan, financing is often viewed through the lens of long-term stability, where borrowers are expected to maintain consistent repayments over time. Cultural factors dictate that financial institutions prioritize thorough vetting of applicants, leading to a very structured borrowing environment.

| Institution | Annual Interest Rate | Loan Amount | Repayment Examples |

|---|---|---|---|

| Mitsubishi UFJ Financial Group (MUFG) | 2.0%–14.5% | Up to 10 million JPY | 1 million JPY at 7% over 5 years: ~19,800 JPY/month |

| Mizuho Bank | 2.0%–14.0% | Up to 10 million JPY | 3 million JPY at 5% over 7 years: ~42,000 JPY/month |

source: [MUFG](https://www.bk.mufg.jp), [Mizuho Bank](https://www.mizuhobank.co.jp)

Conclusion: Making Informed Loan Choices

When engaging in the financial equivalent of a "56d Bet" by deciding on a loan, borrowers should consider risk and reward carefully. Each lending option offers unique terms, benefits, and challenges. Hence, it’s crucial to compare and contrast these offerings to find the best fit for one’s financial situation. Understanding global loan landscapes empowers borrowers to make informed decisions, giving them leverage in negotiations and helping to avoid financial pitfalls. Armed with knowledge, borrowers can approach the loan market with confidence, recognizing that informed choices today can lead to financial stability tomorrow. Additionally, it is wise to remain updated on changing interest rates and economic indicators, as these factors can dramatically influence loan markets and borrower strategies.

Furthermore, integrating these strategies into your overall financial planning can yield significant dividends in the long run. As you position yourself to engage in loans, think critically about your long-term financial health, and ensure that the decisions you make today are in alignment with your broader financial goals. Your ability to navigate the complexities of borrowing can determine not just your immediate financial situation but also impact your future financial security.

FAQs

1. What factors should I consider when choosing a loan?

Analyzing interest rates, repayment terms, total repayable amount, lender credibility, and the fine print about fees and charges is essential when choosing a loan. This also encompasses understanding your own financial health and how a loan fits into that picture.

2. How does one ensure a loan is within their capacity to repay?

Assess your financial stability and budget to ensure monthly repayments are manageable. It’s vital to understand all terms within your financial context. Create a detailed budget that includes all your expenses and how a potential loan repayment fits into that structure.

3. What's the significance of '56d Bet' in personal finance?

It symbolizes a calculated risk in investment strategies or financial decisions, akin to making an informed loan choice based on terms and conditions. It reminds borrowers that every financial decision carries inherent risks; hence, it is vital to weigh the impacts before proceeding.

4. Are there alternatives to traditional loans I should consider?

Yes, options like peer-to-peer lending, personal lines of credit, and credit cards are viable alternatives. Each option carries its pros and cons, making it essential to evaluate what best suits your financial needs.

5. How often should I review my loans or borrowing strategies?

Regularly reviewing your loans, ideally annually, can help you stay informed about your financial health and identify opportunities for refinancing or consolidation that could save money in the long run.

Disclaimer

The above information comes from online resources, and the data is as of October 2023. Specific loan requirements, offerings, and repayment methods are subject to change based on official requirements. This website will not be updated in real-time, and users should verify information before making financial decisions.

Reference Links

- [Harmoney](https://www.harmoney.com.au)

- [TD Bank](https://www.td.com/us/en/personal-banking)

- [Lloyds Bank](https://www.lloydsbank.com)

- [SoFi](https://www.sofi.com)

- [MUFG](https://www.bk.mufg.jp)

- [Mizuho Bank](https://www.mizuhobank.co.jp)

Further Considerations When Taking a Loan

It is crucial for borrowers to understand that each loan application is a commit to financial responsibility. The act of borrowing should align with a comprehensive financial strategy that considers long-term goals, such as home ownership, investment in education, or retirement planning. Engaging in loans without a clear purpose can lead to unnecessary financial strain.

The Role of Credit Scores

Your credit score plays a significant role in borrowing. It reflects your credit history and how likely you are to repay borrowed money. Lenders use this score to assess risk, with higher scores typically yielding better loan terms. Understanding how to manage your credit score effectively can save you money and improve your borrowing capacity.

- Check credit scores annually.

- Pay all monthly bills on time.

- Avoid taking on debt beyond your means.

- Regularly review your credit report for errors.

Understanding Loan Fees

Many loans come with fees that can increase the total cost of borrowing. It is important to identify and understand these fees before signing any agreement. Here are some common fees to be aware of:

- Origination Fee: A one-time fee charged by lenders for processing a loan application.

- Late Payment Fee: A fee for missing a scheduled payment deadline.

- Prepayment Penalty: A fee incurred when paying off a loan early, which could be counterproductive for borrowers looking to minimize interest payments.

- Annual Fees: Ongoing fees associated with maintaining a credit account.

Informed Decision-Making: The Key to Loan Management

In summary, making informed financial decisions regarding loans and borrowing can substantially impact your financial future. The financial landscape is dotted with various options; each will present its unique considerations regarding terms, repayments, and obligations. Bet wisely on your financial future, assess, compare, and strategize to ensure that your loan journey leads to sustainable success rather than risk-laden pitfalls.

-

1

Explore the Tranquil Bliss of Idyllic Rural Retreats

-

2

Unlock the Full Potential of Your RAM 1500: Master the Art of Efficient Towing!

-

3

Leveraging High-Interest CDs for Optimized Investment Returns

-

4

How to Take Advantage of Debt Consolidation Loans: Key Strategies

-

5

Understanding Debt Consolidation Loans: Weighing Advantages and Disadvantages